Patrick Shea Gowlings Laughing about Nortel Lawyers' Fees.mp3

Bankruptcy Proceedings Have Uncontrolled Costs

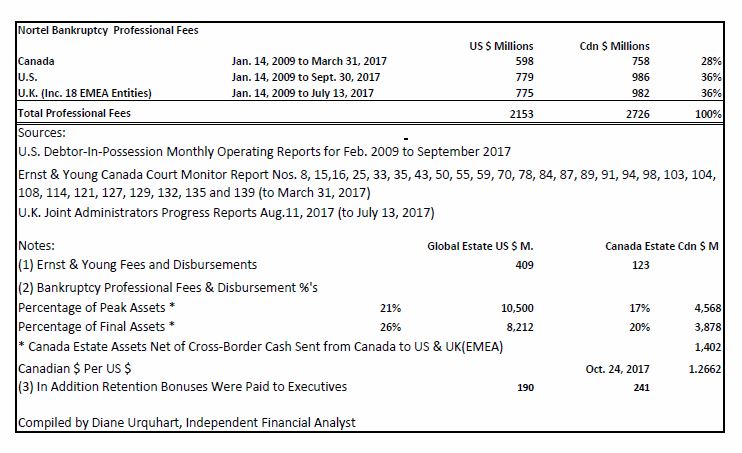

The Nortel bankruptcy is the most expensive court administered large bankruptcy in the history of the world. See tables below.

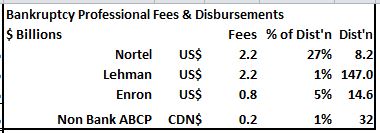

The total Nortel bankruptcy professional fees disclosed as of October 25, 2017 is US$2.2 billion, or 26% of the US$8.2 billion of cash distributed to its creditors. The Nortel CCAA proceeding is still ongoing after almost 9 years to date. 10 Nortel businesses, including the intellectual property patents, were sold between 2009 and 2011. The Nortel global estate had peak assets post bankruptcy filing of US$10.5 billion at 2011. The next 6 years were spent negotiating, mediating and litigating on how the cash should be distributed to the three geographic estates of Canada, US and UK(EMEA).

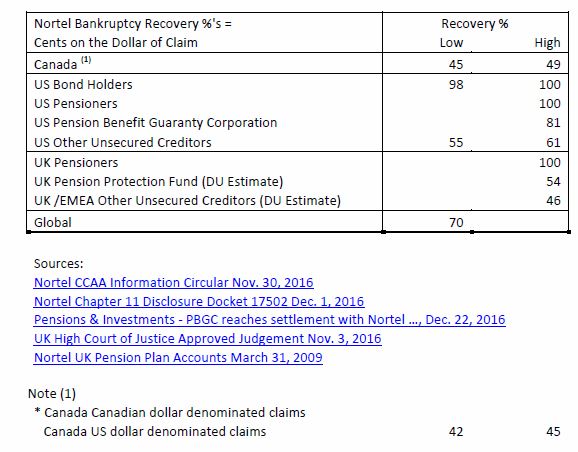

If equal treatment of creditors is the bedrock of insolvency law according to spokespeople for the Insolvency Institute of Canada and given that J. Gross and J. Newbold decided equal treatment of creditors also applies internationally, then what was all this money spent on bankruptcy professionals accomplishing. The Nortel bondholders did get value for their legal costs since they were successful in achieving 100 cents of their dollar of claim, while the Nortel pensioners, disabled and severed employees got just 45 cents. The bond holders got fully paid due to cross-border guaranties in their legal covenants written before the bankruptcy, and due to over US$2.1 billion of cross-border claims placed against the Canada estate that were approved by the judges, before these judges decided equal treatment was the way to go.

The US investment bank, Lehman, also had US$2.2 billion of bankruptcy professional fees, but this was just 1% of the US$147 billion of cash and securities distributed to its creditors. Lehman had over 900,000 derivatives contracts to be resolved, in the course of winding up the Lehman corporate entities.

Canada's largest bankruptcy was Non Bank ABCP, also due to the financial crisis. There were Cdn$199 million of Non Bank ABCP bankruptcy professional fees, which were just 1% of the Cdn$32 billion of cash and securities distributed to its creditors. There were 22 trusts, containing 114 derivative contracts and $3 billion in collateralized debt obligations containing subprime mortgages. Despite the complexity, the Non Bank ABCP CCAA proceeding was completed within 18 months.

It is important to note that Ernst & Young itself received professional fees to date of US$409 million (Cdn$518 million) from the Nortel bankruptcy. Ernst & Young has had three conflicting roles in the Nortel bankruptcy proceeding: Canada Court Monitor (Cdn$123 million), UK/EMEA Court Administrator (Cdn$345 million) and US corporate entities' tax advisor (Cdn$50 million.) The first two of these roles are delegated court administration functions. Most of the US estate cross-border claim against the Canada estate, related to an IRS/CRA Advance Pricing Agreement, that Ernst & Young was surely involved in.

The CCAA sets out the role of the CCAA Court Monitor and its includes:

- send a notice to every known creditor advising them that the CCAA proceeding is underway

- prepare a list of the creditors and amounts of their claims and make it publicly available

- review the company’s cash-flow statement as to its reasonableness and file a report with the court on the monitor’s findings

- make, or cause to be made, any appraisal or investigation the monitor considers necessary to determine with reasonable accuracy the state of the company’s business and financial affairs and file a report with the court on the monitor’s findings

- advise the court on the reasonableness and fairness of any compromise or arrangement that is proposed between the company and its creditors

- make the prescribed documents publicly available in the prescribed manner and at the prescribed time and provide the company’s creditors with information as to how they may access those documents

The above duties could be completed by a court administrator working for the judge and the judge himself finally determines the reasonableness and fairness of any compromise of arrangement, so why is Ernst & Young paid such an exorbitant sum of money, especially if equal treatment of creditors is the so-called bedrock of insolvency law. Plus, how can Canadians place so much confidence in Ernst & Young's role as Court Monitor given its record of regulatory and class action lawsuit settlements for claims of misrepresentations and poor audits done by it, as shown in the button below.